Taking Profit on Singapore REITs: 13% Cash vs 87% Stocks

Taking Profit on Singapore REITs: 13% Cash vs 87% Stocks

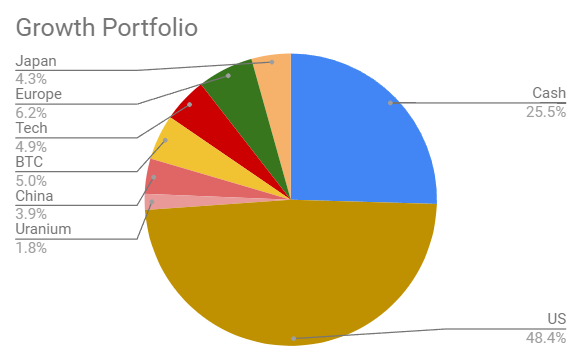

Rotating into a mix of less correlated bets: Europe, Japan, China equities, global tech, uranium and cash.

Singapore REITs have staged a modest rally from the Oct 2023 bottom. They are up about 8.5% as a group.

Hence, I’m taking profit on some REITs. I have reduced their position from 57% to 49.6% in the overall portfolio.

The REITs I have sold are parts of Parkway Life REIT and CapitaLand India Trust.

Why have I reduced exposure to REITs, especially since they should do well when the Fed cuts interest rates later this year?

Reason #1: Reducing portfolio exposure to interest rate risk

The January US CPI figure came in hotter than expected, at an annualized 3.1%, vs. hopes that it would fall below 3%.

Of concern is supercore inflation, which rose at an annualized 4.4%. What is supercore inflation? It strips out the cost of goods, energy and shelter, and largely measures the impact of wage increases in the huge services part of the US economy.

This has led to fears that the Fed may not be able to cut interest rates as much as hoped for, this year.

The market is still pricing in 4 rate cuts by the Fed. The earliest rate cut (more than 50% probability) is estimated by markets to come in around June 2024.

Given the amount of market volatility around CPI and PCE (29 February) data releases, I would like to raise more cash to take advantage of market corrections.

Reason #2: Diversifying income portfolio

The raising of dividends by DBS to an attractively high level suggests that there are other ways to derive dividend income, other than REITs.

With weakening NIMs and loan growth expected in 2024, there should be more chances to build a conservative Singapore bank position this year.

I would also like to diversify into Asian investment grade corporate bond funds that distribute a dividend.

Reason #3: Upsizing growth portfolio; Downsizing income portfolio

The main reason for reducing REITs is to reduce the size of my income portfolio.

There is no free lunch in dividends investing. The distribution of profits to shareholders means that dividend stocks have less to invest in growth. As my retirement income is largely from physical real estate investments, this gives me more flexibility to invest in stocks more for growth and capital appreciation, and less for income.

The best free lunch is still portfolio diversification.

Reason #4: Growing and diversifying growth portfolio into less correlated bets

I’ve diversified sales proceeds into an European equity ETF, a global AI ETF, a Chinese tech ETF, uranium and cash.

I realise that to you, gentle reader, most of these do not look like “flavour of the month” bets.

That is intentional.

The key attribute of these new investments is that they do not hold or are underweight the Magnificent 7 stocks. That means that while I still hold some (not all) of the Mag7, they are sized far, far smaller than in the S&P 500 or the QQQ ETF.

It is important to me to avoid bets that may suffer badly from 2 major risks:

TERMS OF USE: Some of the information on this website may have changed since the time of writing. By continuing to read this article, you agree to be bound by our Terms of Use and Disclaimer and verify any information before taking action.

LEGAL DISCLAIMER: This content is for informational purposes only. You should not construe such information as material for financial, legal, investment or tax advice. Views and opinions expressed by The Family Investor are personal and not meant to constitute advice. In exchange for using this site, you agree not to hold The Family Investor liable for any claims of damages upon decisions you make after visiting this site.