How to get $8,500 monthly after age 65, with as little risk as possible

How to get $8,500 monthly after age 65, with as little risk as possible

Products that give $8,500 payouts are available. You just need a minimum sum of $726,000 per spouse.

You can receive $8,500 a month after age 65, for as little risk as possible. The infrastructure of available products is in place. You only need to optimise your strategy.

However, you need to start planning for it. And you need to know how to stick to your savings plan.

If you find it hard to save $726,000 per spouse in today’s money terms as of age 55, then this strategy isn’t ideal for you. You may have to support yourself with lower monthly payouts or a different strategy involving more risk.

This is a strategy for couples nearing age 55, with at least $726,000 saved per spouse, outside of their residential home.

Can a Regular Joe achieve $726,000 in savings by age 55?

This is probably the most common question to the article above.

The answer is yes. The $726,000 includes CPF contributions by employer and employee.

The table below, from Dollars and Sense SG, shows you the median CPF savings for every age group in Singapore.

Singaporeans aged 50 to 55 have between $300,000 to below $400,000 on median. Let’s take the midpoint of $350,000.

Given that the median Singaporean (or Average Joe) has $350,000 in their CPF savings by age 55, he will need another $726,000 - $350,000 = $376,000.

In other words, by age 55, Average Joe needs to save $376,000 outside of CPF.

Let’s assume that Average Joe spends his 20s earning a low wage and spending all his money on property or living.

Then, at age 30, he finally is stable enough in his career to start putting aside money for a rainy day.

He only needs to put aside $15,040 a year, or $1,253 a month. This can be done either through monthly savings or through his annual bonus.

Is this achievable? The median salary of Average Joe in Singapore is $5,197 in 2023, according to official data from the Labour Force 2023 report. To save $1,253 a month, that is equivalent to a saving rate of 24%. The personal saving rate of Singaporeans stands at 35.2%, as of 4Q2023, according to the Singapore Department of Statistics.

This means that Average Joe should not have too much difficulty saving $1,253 a month, or $15,040 a year.

At this saving rate, Average Joe will achieve about $376,000 outside of his CPF in 25 years.

That is how the Average Joe saves enough to accumulate $726,000 at age 55, including his CPF.

What's next?

There are 4 steps involved in this low-fuss retirement strategy.

Step 1: Get A Life Partner

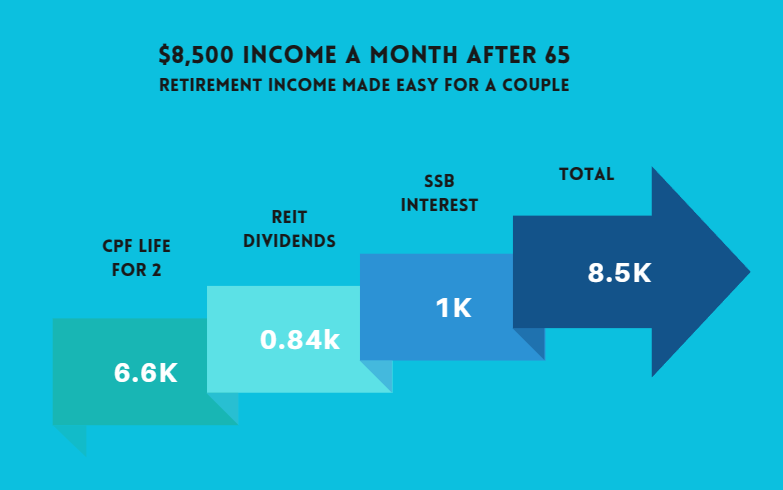

The $8,500 a month in retirement income, after 65, comes by with less risk only if you are part of a couple.

If you are single, you can only receive $4,250 a month in retirement income, using the same strategy.

Step 2: Invest $200,000 per spouse into fixed income like Singapore Savings Bonds, at age 65

Each individual is allowed to have a maximum of $200,000 in Singapore Savings Bonds.

With $200,000 of 10-year SSBs yielding an average of 3%, you will receive $6,000 a year, or $500 a month.

If both spouses buy SSBs up to $200,000 each, the couple will receive $1,000 a month from SSB coupons.

There is reinvestment risk after 10 years. Alternatively, interest rates may drop just as you turn age 65.

If so, you can invest in corporate bond funds. Investment grade corporate bond funds are currently yielding more than 4% after management fees.

Just make sure this is some kind of fixed income instrument.

Step 3: Invest $100,000 per spouse into Singapore REITs.

My preference is for blue-chip REITs rather than dividend stocks in Singapore. This is because you can buy the index and simply forget about active management.

If you prefer dividend stocks, go ahead and do your research. Just remember that if you buy banks, they have an interest rate cycle and can cut back on dividends severely, if mandated by either MAS or their capital requirements.

With $100,000 of Singapore REITs per spouse, and with REITs yielding an average of 5% today, you can receive about $5,000 a year, or $420 per month.

As a couple, you receive about $840 a month from REIT dividends.

You may say that REITs may not yield 5% when you are ready to retire.

You can invest in them when you have the cash, during market cycles when their share prices are trading low, like now. As their share prices are cheap, their yields have risen to about 5% on average.

Step 4: Invest $426,000 into the CPF Enhanced Retirement Sum, per spouse, at age 55

This is the easiest, most risk-free way to get $6,660 a month after age 65, as a couple, for as long as you live.

You each top up to the CPF Enhanced Retirement Sum of $426,000 at age 55 (as of 2025), into your CPF Retirement Account. When each spouse does this, the total payouts generated every month, at age 65, is $6,660 a month. This is a risk-free payout that will continue no matter how long you live.

In other words, it is a perfect hedge for longevity risk.

Retirement income of $8,500 per couple at age 65 is achievable, if you plan.

As the saying goes, if you fail to plan, you plan to fail.

Going by the median CPF savings, median salary and median personal savings rate in Singapore, the Regular Joe can accumulate $726,000 by age 55.

By investing prudently into a mix of Singapore Savings Bonds (fixed income), Singapore REITs (equity) and CPF Life (annuity), retirees can secure their monthly income in a safe and low risk way.

TERMS OF USE: Some of the information on this website may have changed since the time of writing. By continuing to read this article, you agree to be bound by our Terms of Use and Disclaimer and verify any information before taking action.

LEGAL DISCLAIMER: This content is for informational purposes only. You should not construe such information as material for financial, legal, investment or tax advice. Views and opinions expressed by The Family Investor are personal and not meant to constitute advice. In exchange for using this site, you agree not to hold The Family Investor liable for any claims of damages upon decisions you make after visiting this site.